Insurance Education

Why “Should I Call My Insurance Agent?” Is a Question With Only One Answer

We’ve all been there. You’re staring at a new piece of mail, considering a minor home renovation, or wondering if your side hustle needs its

Purchasing the right insurance is a crucial step for any startup, but it can often get overlooked by busy founders focused on product-market fit and funding rounds. This comprehensive guide outlines the essential coverages startups need, how much they cost, and tips for choosing insurance providers tailored to the unique risks facing young tech companies and entrepreneurs.

Launching a startup involves calculated risks, but exposing your personal assets or the future of your company to potential lawsuits or liability claims doesn’t need to be one of them. The right insurance coverages help founders transfer many risks away from the business through affordable monthly premiums.

Here are some key reasons obtaining startup insurance should be a priority:

While risks certainly vary across companies, these core insurance policies protect against the most common startup exposures.

This fundamental coverage protects against premises liability, product liability, copyright infringement, reputational harm from reviews, and more. For example, if a client slipped and suffered an injury at your office.

If your startup sells software or provides consulting services, this coverage is crucial. It responds to lawsuits alleging your professional advice or products caused financial harm due to negligence, errors, misleading statements, or failure to safeguard client data properly.

Hackers and cyber extortionists actively target startups to steal funds and data. Having robust first- and third-party digital liability coverage is essential to survive these incidents.

Shareholders, investors, competitors, vendors, and employees can all potentially sue startup directors and officers over their business decisions alleging mismanagement or negligence. D&O insurance is the only asset shield for these individuals.

Table 1: Comprehensive Breakdown of Startup Insurance Policies

Stage | Risks/Exposures | Recommended Policies | What It Covers | Estimated Cost |

Pre-launch | Personal assets at risk, founder/investor lawsuits | Directors & Officers (D&O) Insurance | Lawsuits against directors and officers alleging mismanagement or negligence | $1,500 annually |

Early Traction | Client lawsuits, failure to deliver services, professional mistakes | Errors & Omissions Insurance | Lawsuits from customers related to work quality, missed deadlines, negligent advice | $100 – $300 monthly |

First Office | Commercial property damage, equipment theft | Commercial Property Insurance | Damage to office space, furnishings, computers, equipment, and other business property | $100 – $500 monthly |

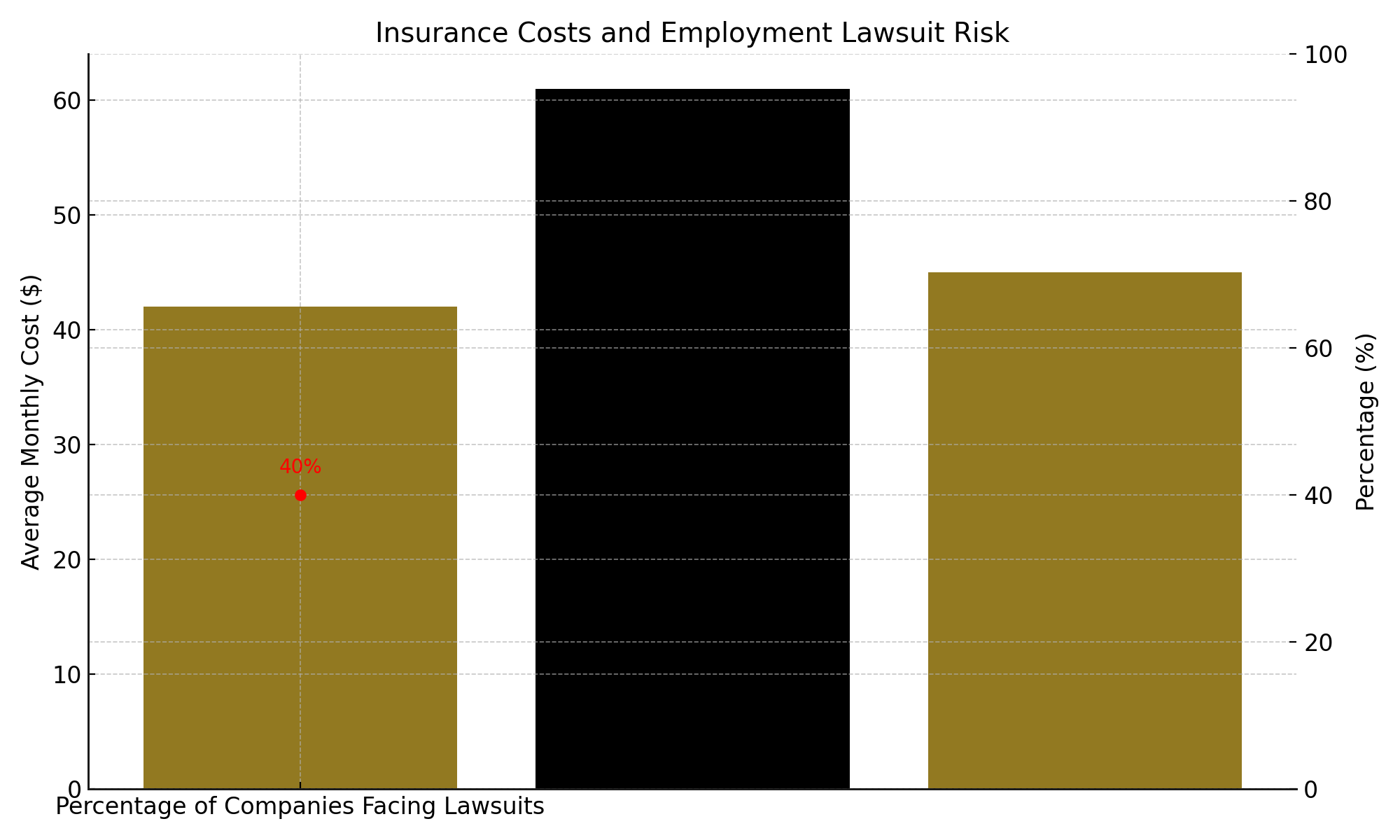

First Hires | Workplace injuries, employment lawsuits | Employment Practices Liability Insurance | Claims of discrimination, sexual harassment, wrongful termination | $50+ monthly |

Post-Funding | Increased cyber risks, crime exposures, growth risks | Cyber Liability Insurance | Data breaches, hacking incidents, cyber extortion threats | $100+ monthly |

While the policies above cover the most common startup risks, additional insurance should be considered for certain situations:

The average monthly costs for key startup policies are:

Of course, costs vary widely based on your startup’s size, location, and industry risk profile. However, allocating even 1-3% of your annual revenue to insurance can pay dividends by letting you focus on innovation rather than litigation threats.

Table 2: Startup Insurance Cost Estimates by Company Stage

Stage | Est. Revenue | Recommended Insurance Investment | Est. Total Insurance Costs |

Pre-Seed | Under $50K | 1-2% of Revenue | $500 – $1,000 annually |

Seed Funded | $50K – $500K | 1-3% of Revenue | $1,000 – $15,000 annually |

Series A | $500K – $5M | 1-5% of Revenue | $5,000 – $250,000 annually |

Series B+ | Over $5M | 1-6% of Revenue | $50,000+ annually |

Here are a few tips to make getting properly insured smooth and cost-effective:

Work with specialized agents/brokers: The best startup insurance brokers have worked with hundreds of emerging tech companies and understand the unique risks. They can tailor broader packages efficiently.

Ask about discounts for risk mitigation: Some insurers offer discounted premiums if startups implement formal cyber security and employee conduct safeguards.

Bundle multiple policies: Bundling similar policies together or with health/benefits plans can lead to policy discounts. A good agent helps coordinate this.

Compare quotes: Be wary of only getting one insurance quote. Responsible comparison shopping for the same or better protection can minimize costs.

Table 3: Policy Bundling Opportunities for Startup Insurance

Bundle | Combined Policies | Average Savings |

Tech Package | Cyber Liability, Tech E&O | 10-20% |

Management Liability | Directors & Officers, Employment Practices Liability | 15%+ |

Business Owner’s Policy (BOP) | General Liability, Commercial Property, Business Interruption | 10-30% |

As an independent insurance agency serving Connecticut for over 12 years, Branco Insurance Group has the experience to find the right insurance solutions for startups and small businesses. Whether you need general liability, professional liability, cyber insurance, or customized packages, our agents take the time to understand your company’s specific risks and growth plans so we can tailor coverage accordingly. We represent over 25 top-rated insurers to fit your budget at every stage.

If you’re a young company needing guidance on insurance requirements, risk management planning, or attracting investors, let’s have a consultation. We can outline options to safely transfer risk away from your startup’s future so you can focus on sustaining innovation. Our past clients confirm working with Branco gives entrepreneurs like you peace of mind and financial safeguards to enable that next big breakthrough. Contact us today to see how we can help.

We’ve all been there. You’re staring at a new piece of mail, considering a minor home renovation, or wondering if your side hustle needs its

Spring Brings Momentum—and Risk Spring is busy for small businesses. Foot traffic picks up, projects ramp up, and operations move faster. With all that momentum,